The Paris-based company also expects capacity demand to be multiplied by a factor of 13. Capacity revenues will be boosted from $10.2b in 2021 to $22.4b in 2031, it says, despite falling capacity prices.

Services revenue

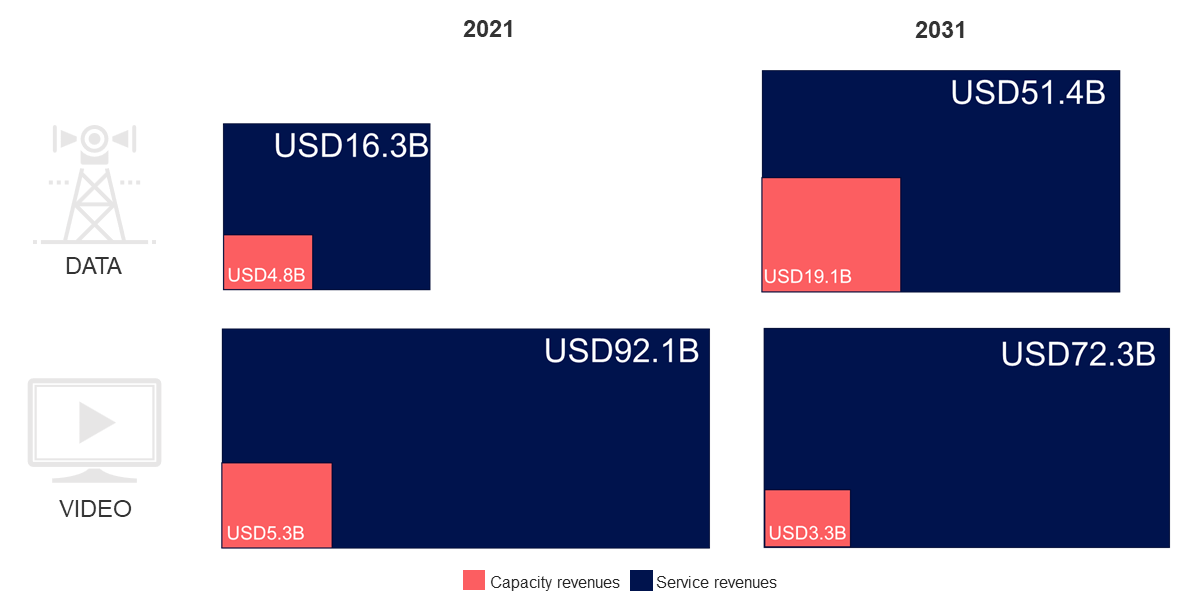

In terms of satellite services revenue, it says we are likely to see an “explosion” of revenue to the tune of a cumulative $1.2 trillion by 2031. It forecasts the share of data applications increasing from 15% of total market revenues to 42% by 2031.

“A falling average revenue per user (ARPU) and a fiercely competitive market have been the main drivers for changes in strategies, with operators pushed to look for extra revenues to avoid the commodity price trap. Their sights have been increasingly set on a new revenue stream – Services – which will grow from $108 billion to $124 billion in the space of 10 years, with all the growth coming from data services.”

“The shift towards data-driven revenue streams can also be seen in the downward trend of video revenues, with the projected loss of 26 million direct-to-home (DTH) subscribers and 8,500 satellite TV channels by 2031. Changes in viewing habits will contribute to the growing shift from linear viewing to Over-the-Top (OTT) services that will negatively impact the satellite video market in coming years.”

NGSO

Euroconsult also highlights the the disruptive effect of Non-Geostationary Orbit Satellites (NGSOs).

“The rapidly growing importance of NGSO in connectivity markets is heavily impacting the FSS industry, with an increasing number of players looking at a multi-orbit strategy to expand their business, as highlighted by Eutelsat’s recently announced merger with OneWeb, and the endeavours of several FSS operators to create a European NGSO constellation.”

The graphic above pictures capacity revenues and service revenues, for both data and video.

“However,” the company notes, “COVID-19 and the war in Ukraine have not spared the FSS (fixed satellite services) industry, with supply chain issues due to microprocessor shortages and manufacturing bottlenecks leading to a significant number of satellites being delayed. The global inflation crisis has also pushed up satellite prices, most visibly impacting NGSO constellations like Telesat’s Lightspeed, which was forced to downsize.”

“Despite these short-term setbacks, the industry is expected to have a capacity revenue growth of 5% year-over-year in 2022, with the next launches of new constellations and large satellites in coming years being likely to kick off the period of growth by opening the floodgates of new capacity.”

See also: Government budgets for space exploration and militarisation hit record levels